CP26/28 is the biggest shake-up of UK alternative asset management regulation since AIFMD itself arrived.

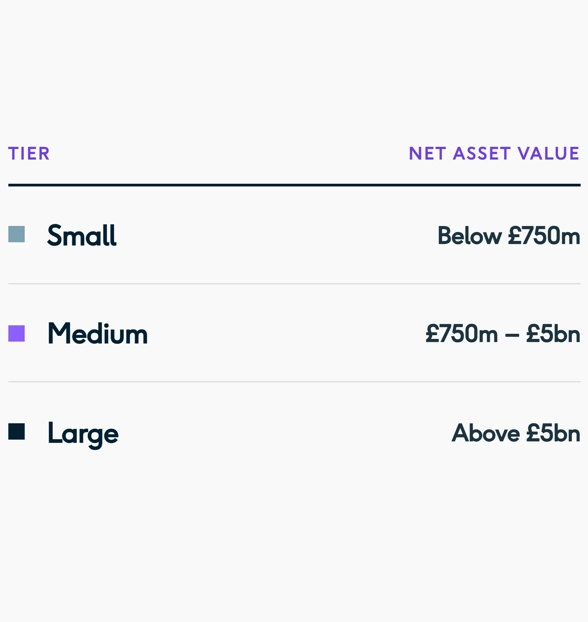

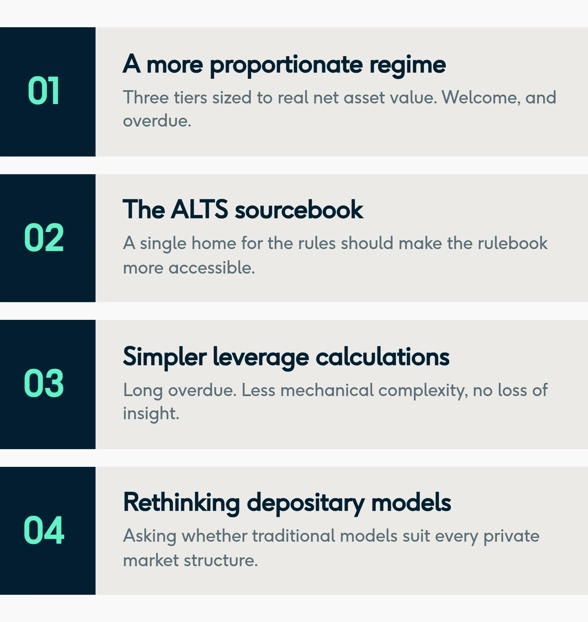

Published on 14 July 2026, the FCA's consultation gets a lot right - starting with a proportionate three-tier regime based on net asset value, not leveraged assets under management.

Alongside the tiers, the consultation proposes simpler leverage calculations, principles-based disclosure, less duplicated trust reporting and flexible depositary arrangements. All sensible ambitions.

These proposals do not stand alone. They run in parallel with an HM Treasury consultation on the underlying AIFMD derived statutes, a top down overhaul that moves key rule making powers from the statute book straight to the FCA. A nimbler framework, yes. But also a more powerful regulator. That is exactly why engagement matters.

Do not judge a consultation of this scale on its headlines. Regulation should protect investors and support efficient markets. Too often, it has become one of the largest drivers of unnecessary cost and complexity instead. The UK has a habit of over-engineering rules that begin with simple objectives and parts of CP26/28 risk repeating that pattern even as they try to fix it.

Reopening the perimeter

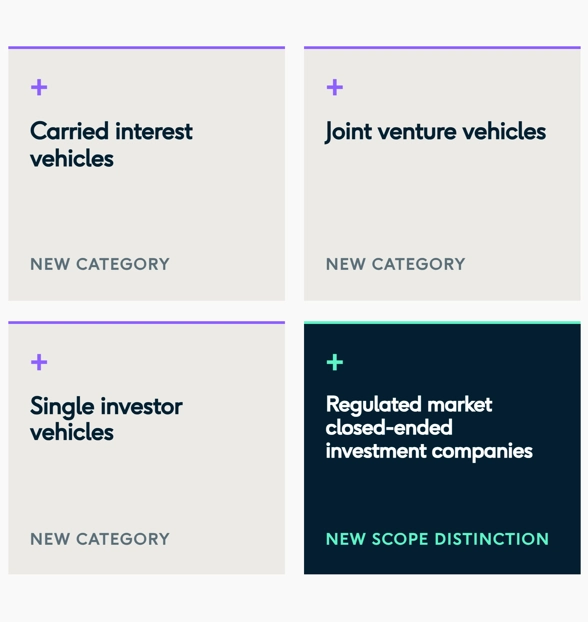

The clearest warning sign: the renewed effort to redraw the perimeter of what constitutes an 'AIF'. The proposals introduce new categories and scope distinctions.

None objectionable in themselves. But they land in an area of regulation that took more than a decade to become operationally understood.

Scope has never been simple. Before AIFMD even took effect, policymakers were asking whether the concept of an AIF was clear enough.

The UK's Financial Markets Law Committee said in 2010 that the term had no settled meaning; similar concerns echoed across Europe. The root problem: 'fund' was never a single economic concept. To a wealth manager, a fund is a packaged product designed for distribution to end investors. In private markets, it is a legal and organisational framework through which sophisticated institutions co-invest.

Those concerns were never resolved. Instead, industry, advisers and regulators spent a decade building a broadly accepted, if imperfect, understanding of what an AIF is in practice.

That understanding has value. It underpins legal opinions, fund documentation, regulatory filings, investor disclosures and operating models across jurisdictions.

Reopening the definition on a UK-only basis risks disturbing a hard-won consensus which, despite its imperfections, has become operationally workable.

The cost of divergence

The cost lands hardest in cross-border fundraising. Managers already navigate national private placement regimes, reverse solicitation rules and divergent readings of AIFMD just to raise capital from counterparts that need little protection. The last thing the industry needs is another layer of UK–EU divergence. If a structure can be characterised differently on either side of the Channel, expect more legal analysis, revised investor documentation, separate marketing assessments and bespoke disclosures. None of that improves investor outcomes. It adds cost, slows execution and creates friction in a market where international coherence should be a competitive advantage.

And with the Government seeking closer cooperation with European partners, new regulatory barriers to cross-border business look like the wrong reform at the wrong time.

What deserves support

None of this should drown out what is genuinely good in CP26/28 and industry should say so.

This is a regulator increasingly prepared to accept that private markets are not just a variation of public markets.

The most interesting signal may be about the future of private capital oversight. The FCA's depositary discussion acknowledges that private equity, private credit, infrastructure and real estate funds do not always fit models built for traditional custodial assets. No conclusions yet - but the direction of travel points towards more risk-based, proportionate investor protection in private markets.

The operational lens

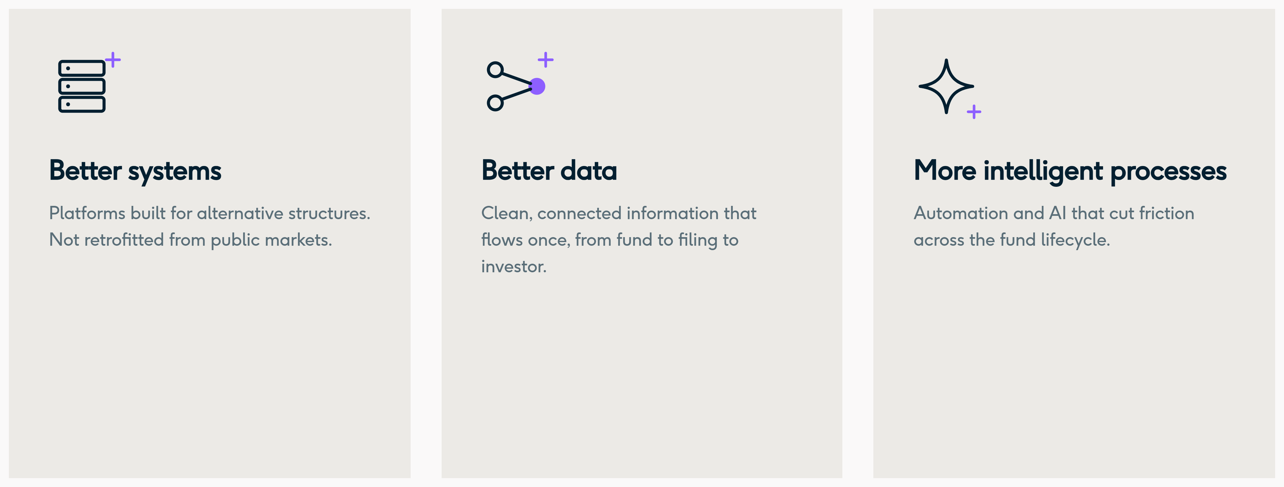

At Palmer, we look at this through both a regulatory and an operational lens. As a technology driven fund administrator for alternative asset managers, we see it first-hand.

The biggest wins will come where clearer rules meet three things:

The goal is not fewer rules for their own sake, it is a framework that lets managers, investors and service providers operate more efficiently, use information better and cut friction across the fund lifecycle.

Support what simplifies. Challenge what complicates. Engage before the framework is fixed.